协方差:两个变量总体误差的期望。

简单的说就是度量Y和X之间关系的方向和强度。

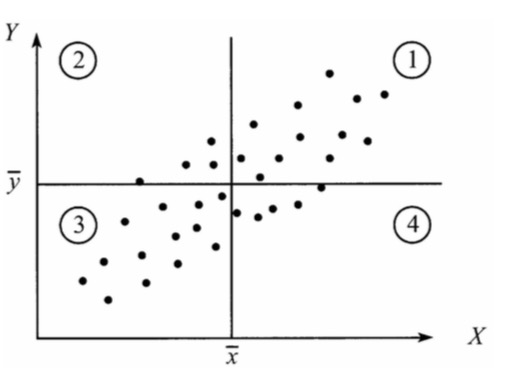

X :预测变量

Y :响应变量

Y和X的协方差:[来度量各个维度偏离其均值的程度]

备注:[之所以除以n-1而不是除以n,是因为这样能使我们以较小的样本集更好的逼近总体的协方差,即统计上所谓的“无偏估计”。而方差则仅仅是标准差的平方]

如果结果为正值,则说明两者是正相关的(从协方差可以引出“相关系数”的定义),

如果结果为负值就说明负相关的

如果为0,也是就是统计上说的“相互独立”

为什么呢:

如果第1,3象限点位多,最终的和就是正,X增大Y增大

如果第2,4象限点位多,最终的和就是负,X增大Y减小

Cov(Y,X)会受到度量单位的影响

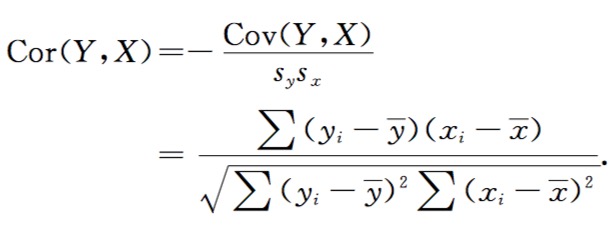

引入相关系数:

![]()

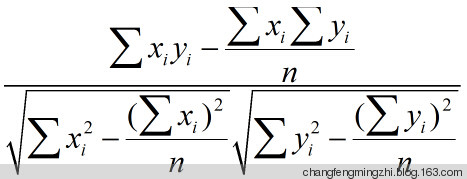

python使用以下公式进行计算[上面的公式不便于编程,需要多次扫描数据,但是微小的错误会被放大哦]:

#coding:utf-8

‘‘‘

Y和X的相关系数就是标准化后变量的协方差

‘‘‘

‘‘‘

__author__ = ‘similarface‘

QQ:841196883@qq.com

‘‘‘

from math import sqrt

from pandas import *

import pandas as pd

import os,sys

import matplotlib.pyplot as plt

#安装不了 就github下载源码安装

from sklearn import datasets, linear_model

‘‘‘

根据文件加载数据

‘‘‘

def loaddataInTab(filename):

if os.path.isfile(filename):

try:

return pd.read_table(filename)

except Exception,e:

print(e.message)

else:

print("文件存在!")

return None

‘‘‘

获取Y,X的相关系数,即为:皮尔逊相关系数

‘‘‘

def pearson(rating1, rating2):

‘‘‘

皮尔逊相关参数

在统计学中,皮尔逊积矩相关系数

(英语:Pearson product-moment correlation coefficient,

又称作 PPMCC或PCCs[1],

文章中常用r或Pearson‘s r表示)

用于度量两个变量X和Y之间的相关(线性相关),其值介于-1与1之间。

在自然科学领域中,该系数广泛用于度量两个变量之间的相关程度。

0.8-1.0 极强相关

0.6-0.8 强相关

0.4-0.6 中等程度相关

0.2-0.4 弱相关

0.0-0.2 极弱相关或无相关

‘‘‘

sum_xy, sum_x, sum_y, sum_x2, sum_y2, n = 0, 0, 0, 0, 0, 0

for i in xrange(len(rating1)):

n = n + 1

x = rating1[i]

y = rating2[i]

sum_xy += x * y

sum_x += x

sum_y += y

sum_x2 += x ** 2

sum_y2 += y ** 2

if n == 0:

return 0

fenmu = sqrt(sum_x2 - (sum_x ** 2) / n) * sqrt(sum_y2 - (sum_y ** 2) / n)

if fenmu == 0:

return 0

else:

return (sum_xy - (sum_x * sum_y) / n) / fenmu

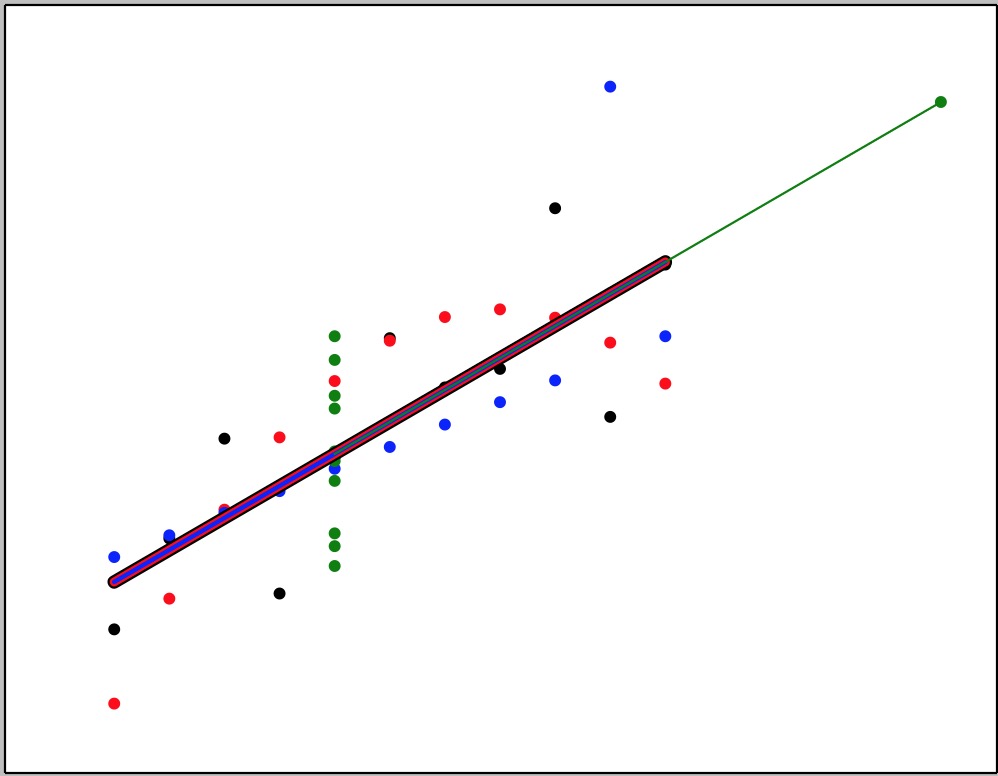

data=loaddataInTab(‘./AnscombeQuartet‘)

#x1,y1是线性相关的

diabetes_x1_test=data[‘X1‘]

diabetes_y1_test=data[‘Y1‘]

plt.scatter(diabetes_x1_test, diabetes_y1_test, color=‘black‘)

print("黑色点的相关系数为:{}(皮尔逊相关参数)".format(pearson(diabetes_x1_test,diabetes_y1_test)))

regr1 = linear_model.LinearRegression()

diabetes_x1_train=diabetes_x1_test.as_matrix()[:, np.newaxis]

diabetes_y1_train=diabetes_y1_test.as_matrix()[:, np.newaxis]

regr1.fit(diabetes_x1_train, diabetes_y1_train)

plt.plot(diabetes_x1_test.as_matrix()[:, np.newaxis], regr1.predict(diabetes_x1_test.as_matrix()[:, np.newaxis]), color=‘black‘,linewidth=6)

#x2,y2是非线性 二次函数拟合

diabetes_x2_test=data[‘X2‘]

diabetes_y2_test=data[‘Y2‘]

plt.scatter(diabetes_x2_test, diabetes_y2_test, color=‘red‘)

print("红色点的相关系数为:{}(皮尔逊相关参数)".format(pearson(diabetes_x2_test,diabetes_y2_test)))

regr2 = linear_model.LinearRegression()

diabetes_x2_train=diabetes_x2_test.as_matrix()[:, np.newaxis]

diabetes_y2_train=diabetes_y2_test.as_matrix()[:, np.newaxis]

regr2.fit(diabetes_x2_train, diabetes_y2_train)

plt.plot(diabetes_x2_test.as_matrix()[:, np.newaxis], regr2.predict(diabetes_x2_test.as_matrix()[:, np.newaxis]), color=‘red‘,linewidth=4)

#x3,y3 数据对中出现了 孤立点

diabetes_x3_test=data[‘X3‘]

diabetes_y3_test=data[‘Y3‘]

plt.scatter(diabetes_x3_test, diabetes_y3_test, color=‘blue‘)

print("蓝色点的相关系数为:{}(皮尔逊相关参数)".format(pearson(diabetes_x3_test,diabetes_y3_test)))

regr3 = linear_model.LinearRegression()

diabetes_x3_train=diabetes_x3_test.as_matrix()[:, np.newaxis]

diabetes_y3_train=diabetes_y3_test.as_matrix()[:, np.newaxis]

regr3.fit(diabetes_x3_train, diabetes_y3_train)

plt.plot(diabetes_x3_test.as_matrix()[:, np.newaxis], regr3.predict(diabetes_x3_test.as_matrix()[:, np.newaxis]), color=‘blue‘,linewidth=2)

#x4,y4不适合线性拟合 极端值确立了直线

diabetes_x4_test=data[‘X4‘]

diabetes_y4_test=data[‘Y4‘]

plt.scatter(diabetes_x4_test, diabetes_y4_test, color=‘green‘)

print("绿色点的相关系数为:{}(皮尔逊相关参数)".format(pearson(diabetes_x4_test,diabetes_y4_test)))

regr4 = linear_model.LinearRegression()

diabetes_x4_train=diabetes_x4_test.as_matrix()[:, np.newaxis]

diabetes_y4_train=diabetes_y4_test.as_matrix()[:, np.newaxis]

regr4.fit(diabetes_x4_train, diabetes_y4_train)

plt.plot(diabetes_x4_test.as_matrix()[:, np.newaxis], regr4.predict(diabetes_x4_test.as_matrix()[:, np.newaxis]), color=‘green‘,linewidth=1)

plt.xticks(())

plt.yticks(())

plt.show()

‘‘‘

把上面的4组数据去做线性回归:

有图可知都做出了,斜率和截距相等的拟合线性

4种X,Y的相关系数都很接近

在解释相关系数之前,图像点位的散点分布是很重要的

如果完全基于相关系数分析数据,将无法发现数据构造模式之间的差别

‘‘‘

参考数据:

1 2 3 4 5 6 7 8 9 10 11 12 | Y1 X1 Y2 X2 Y3 X3 Y4 X48.04 10 9.14 10 7.46 10 6.58 86.95 8 8.14 8 6.77 8 5.76 87.58 13 8.74 13 12.74 13 7.71 88.81 9 8.77 9 7.11 9 8.84 88.33 11 9.26 11 7.81 11 8.47 89.96 14 8.1 14 8.84 14 7.04 87.24 6 6.13 6 6.08 6 5.25 84.26 4 3.1 4 5.39 4 12.5 1910.84 12 9.13 12 8.15 12 5.56 84.82 7 7.26 7 6.42 7 7.91 85.68 5 4.74 5 5.73 5 6.89 8 |

实例:计算机维修

#coding:utf-8

‘‘‘

实例:计算机维修

维修时间 零件个数

Minutes Units

1

...

‘‘‘

__author__ = ‘similarface‘

from math import sqrt

from pandas import *

import pandas as pd

import os

import matplotlib.pyplot as plt

#安装不了 就github下载源码安装

from sklearn import datasets, linear_model

‘‘‘

根据文件加载数据

‘‘‘

def loaddataInTab(filename):

if os.path.isfile(filename):

try:

return pd.read_table(filename)

except Exception,e:

print(e.message)

else:

print("文件存在!")

return None

‘‘‘

获取Y,X的相关系数,即为:皮尔逊相关系数

‘‘‘

def pearson(rating1, rating2):

‘‘‘

皮尔逊相关参数

‘‘‘

sum_xy, sum_x, sum_y, sum_x2, sum_y2, n = 0, 0, 0, 0, 0, 0

for i in xrange(len(rating1)):

n = n + 1

x = rating1[i]

y = rating2[i]

sum_xy += x * y

sum_x += x

sum_y += y

sum_x2 += x ** 2

sum_y2 += y ** 2

if n == 0:

return 0

fenmu = sqrt(sum_x2 - (sum_x ** 2) / n) * sqrt(sum_y2 - (sum_y ** 2) / n)

if fenmu == 0:

return 0

else:

return (sum_xy - (sum_x * sum_y) / n) / fenmu

def getCovariance(XList,YList):

‘‘‘

获取协方差

‘‘‘

averageX=sum(XList)/float(len(XList))

averageY=sum(YList)/float(len(YList))

sumall=0.0

for i in xrange(len(XList)):

sumall=sumall+(XList[i]-averageX)*(YList[i]-averageY)

cov=sumall/(len(XList)-1)

return cov

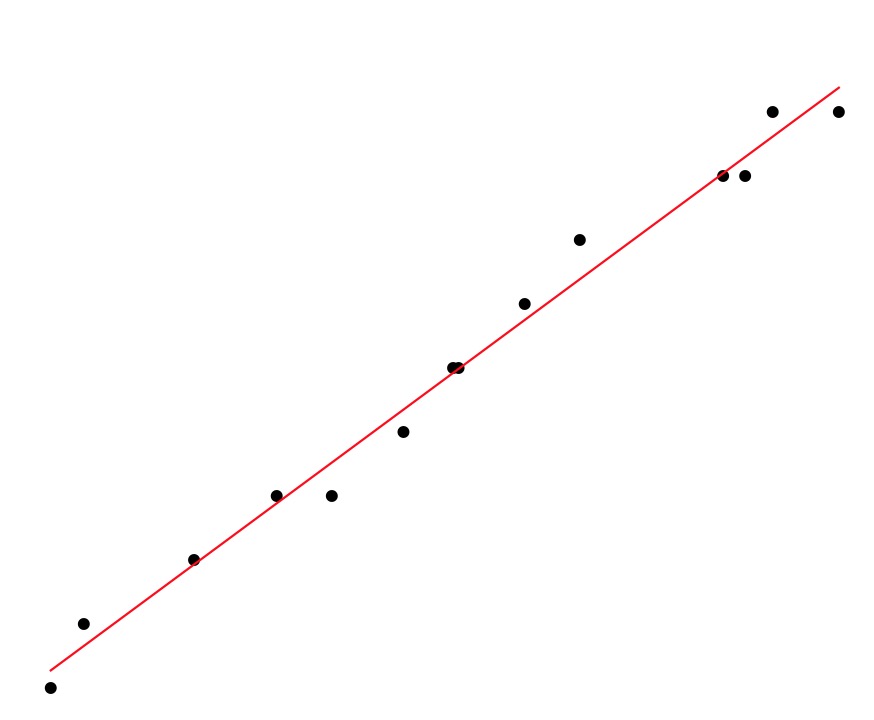

computerrepairdata=loaddataInTab(‘./data/computerrepair.data‘)

Minutes=computerrepairdata[‘Minutes‘]

Units=computerrepairdata[‘Units‘]

print("该数据集的协方差:{}".format(getCovariance(Minutes,Units)))

print("该数据集相关系数:{}".format(pearson(Minutes,Units)))

#维修时间 元件个数散点图

plt.scatter(Minutes, Units, color=‘black‘)

regr = linear_model.LinearRegression()

Minutes_train=Minutes.as_matrix()[:, np.newaxis]

Units_train=Units.as_matrix()[:, np.newaxis]

regr.fit(Minutes_train, Units_train)

print "相关信息"

print("==================================================")

print("方程斜率:{}".format(regr.coef_))

print("方程截距:{}".format(regr._residues))

print("回归方程:y={}x+{}".format(regr.coef_[0][0],regr._residues[0]))

print("==================================================")

plt.plot(Minutes_train, regr.predict(Minutes_train), color=‘red‘,linewidth=1)

plt.xticks(())

plt.yticks(())

plt.show()

result:

该数据集的协方差:136.0

该数据集相关系数:0.993687243916

相关信息

==================================================

方程斜率:[[ 0.06366959]]

方程截距:[ 1.43215942]

回归方程:y=0.0636695930877x+1.43215942092

==================================================

===============参数估计=================

上面的斜率和截距如何算出来的?

简单线性回归模型:

Y=β0+β1X+ε

β0:常数项目

β1:回归系数

ε:随机扰动或误差[除X和Y的线性关系之外的随机因素对Y的影响]

单个观测:

![]()

yi是响应变量的第i个观测值,xi是X的第i个预测值

误差表达式:

![]()

铅直距离平方和:[真实响应变量-预测响应变量]的平方和[最小二乘法]

![]()

使得上诉公式最小值的β[0,1]即为所求的

![]()

直接给出该式的参数解:

其中![]() 带入化简:

带入化简:

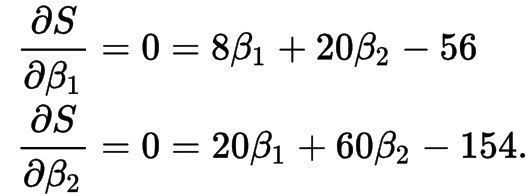

算最小2乘法的例子:

(x,y):(1,6),(2,5),(3,7),(4,10)

假设:y=β1+β2x

β1+1β2=6

β1+2β2=5

β1+3β2=7

β1+4β2=10

得铅直距离方:

化简:

注:这个地方使用了编导数,凹曲面上的极值点在切线斜率为0处

转化成2维面

就解2元1次方程组 一个为3.5 一个为1.4

使用公式计算:

β2=(1-2.5)*(6-7)+(2-2.5)*(5-7)+(3-2.5)(7-7)+(4-2.5)(10-7)/[(1-2.5)(1-2.5)+(2-2.5)(2-2.5)

+(3-2.5)(3-2.5)+(4-2.5)(4-2.5)]=7/5=1.4

python代码计算:

def lsqr(A, b, damp=0.0, atol=1e-8, btol=1e-8, conlim=1e8,

iter_lim=None, show=False, calc_var=False): """Find the least-squares solution to a large, sparse, linear system

of equations.

The function solves ``Ax = b`` or ``min ||b - Ax||^2`` or

``min ||Ax - b||^2 + d^2 ||x||^2``.

The matrix A may be square or rectangular (over-determined or

under-determined), and may have any rank.

::

1. Unsymmetric equations -- solve A*x = b

2. Linear least squares -- solve A*x = b

in the least-squares sense

3. Damped least squares -- solve ( A )*x = ( b )

( damp*I ) ( 0 )

in the least-squares sense

Parameters

----------

A : {sparse matrix, ndarray, LinearOperatorLinear}

Representation of an m-by-n matrix. It is required that

the linear operator can produce ``Ax`` and ``A^T x``.

b : (m,) ndarray

Right-hand side vector ``b``.

damp : float

Damping coefficient.

atol, btol : float

Stopping tolerances. If both are 1.0e-9 (say), the final

residual norm should be accurate to about 9 digits. (The

final x will usually have fewer correct digits, depending on

cond(A) and the size of damp.)

conlim : float

Another stopping tolerance. lsqr terminates if an estimate of

``cond(A)`` exceeds `conlim`. For compatible systems ``Ax =

b``, `conlim` could be as large as 1.0e+12 (say). For

least-squares problems, conlim should be less than 1.0e+8.

Maximum precision can be obtained by setting ``atol = btol =

conlim = zero``, but the number of iterations may then be

excessive.

iter_lim : int

Explicit limitation on number of iterations (for safety).

show : bool

Display an iteration log.

calc_var : bool

Whether to estimate diagonals of ``(A‘A + damp^2*I)^{-1}``.

Returns

-------

x : ndarray of float

The final solution.

istop : int

Gives the reason for termination.

1 means x is an approximate solution to Ax = b.

2 means x approximately solves the least-squares problem.

itn : int

Iteration number upon termination.

r1norm : float

``norm(r)``, where ``r = b - Ax``.

r2norm : float

``sqrt( norm(r)^2 + damp^2 * norm(x)^2 )``. Equal to `r1norm` if

``damp == 0``.

anorm : float

Estimate of Frobenius norm of ``Abar = [[A]; [damp*I]]``.

acond : float

Estimate of ``cond(Abar)``.

arnorm : float

Estimate of ``norm(A‘*r - damp^2*x)``.

xnorm : float

``norm(x)``

var : ndarray of float

If ``calc_var`` is True, estimates all diagonals of

``(A‘A)^{-1}`` (if ``damp == 0``) or more generally ``(A‘A +

damp^2*I)^{-1}``. This is well defined if A has full column

rank or ``damp > 0``. (Not sure what var means if ``rank(A)

< n`` and ``damp = 0.``)

Notes

-----

LSQR uses an iterative method to approximate the solution. The

number of iterations required to reach a certain accuracy depends

strongly on the scaling of the problem. Poor scaling of the rows

or columns of A should therefore be avoided where possible.

For example, in problem 1 the solution is unaltered by

row-scaling. If a row of A is very small or large compared to

the other rows of A, the corresponding row of ( A b ) should be

scaled up or down.

In problems 1 and 2, the solution x is easily recovered

following column-scaling. Unless better information is known,

the nonzero columns of A should be scaled so that they all have

the same Euclidean norm (e.g., 1.0).

In problem 3, there is no freedom to re-scale if damp is

nonzero. However, the value of damp should be assigned only

after attention has been paid to the scaling of A.

The parameter damp is intended to help regularize

ill-conditioned systems, by preventing the true solution from

being very large. Another aid to regularization is provided by

the parameter acond, which may be used to terminate iterations

before the computed solution becomes very large.

If some initial estimate ``x0`` is known and if ``damp == 0``,

one could proceed as follows:

1. Compute a residual vector ``r0 = b - A*x0``.

2. Use LSQR to solve the system ``A*dx = r0``.

3. Add the correction dx to obtain a final solution ``x = x0 + dx``.

This requires that ``x0`` be available before and after the call

to LSQR. To judge the benefits, suppose LSQR takes k1 iterations

to solve A*x = b and k2 iterations to solve A*dx = r0.

If x0 is "good", norm(r0) will be smaller than norm(b).

If the same stopping tolerances atol and btol are used for each

system, k1 and k2 will be similar, but the final solution x0 + dx

should be more accurate. The only way to reduce the total work

is to use a larger stopping tolerance for the second system.

If some value btol is suitable for A*x = b, the larger value

btol*norm(b)/norm(r0) should be suitable for A*dx = r0.

Preconditioning is another way to reduce the number of iterations.

If it is possible to solve a related system ``M*x = b``

efficiently, where M approximates A in some helpful way (e.g. M -

A has low rank or its elements are small relative to those of A),

LSQR may converge more rapidly on the system ``A*M(inverse)*z =

b``, after which x can be recovered by solving M*x = z.

If A is symmetric, LSQR should not be used!

Alternatives are the symmetric conjugate-gradient method (cg)

and/or SYMMLQ. SYMMLQ is an implementation of symmetric cg that

applies to any symmetric A and will converge more rapidly than

LSQR. If A is positive definite, there are other implementations

of symmetric cg that require slightly less work per iteration than

SYMMLQ (but will take the same number of iterations).

References

----------

.. [1] C. C. Paige and M. A. Saunders (1982a).

"LSQR: An algorithm for sparse linear equations and

sparse least squares", ACM TOMS 8(1), 43-71.

.. [2] C. C. Paige and M. A. Saunders (1982b).

"Algorithm 583. LSQR: Sparse linear equations and least

squares problems", ACM TOMS 8(2), 195-209.

.. [3] M. A. Saunders (1995). "Solution of sparse rectangular

systems using LSQR and CRAIG", BIT 35, 588-604. """

A = aslinearoperator(A) if len(b.shape) > 1:

b = b.squeeze()

m, n = A.shape if iter_lim is None:

iter_lim = 2 * n

var = np.zeros(n)

msg = (‘The exact solution is x = 0 ‘, ‘Ax - b is small enough, given atol, btol ‘, ‘The least-squares solution is good enough, given atol ‘, ‘The estimate of cond(Abar) has exceeded conlim ‘, ‘Ax - b is small enough for this machine ‘, ‘The least-squares solution is good enough for this machine‘, ‘Cond(Abar) seems to be too large for this machine ‘, ‘The iteration limit has been reached ‘)

itn = 0

istop = 0

nstop = 0

ctol = 0 if conlim > 0:

ctol = 1/conlim

anorm = 0

acond = 0

dampsq = damp**2

ddnorm = 0

res2 = 0

xnorm = 0

xxnorm = 0

z = 0

cs2 = -1

sn2 = 0 """

Set up the first vectors u and v for the bidiagonalization.

These satisfy beta*u = b, alfa*v = A‘u. """

__xm = np.zeros(m) # a matrix for temporary holding

__xn = np.zeros(n) # a matrix for temporary holding

v = np.zeros(n)

u = b

x = np.zeros(n)

alfa = 0

beta = np.linalg.norm(u)

w = np.zeros(n) if beta > 0:

u = (1/beta) * u

v = A.rmatvec(u)

alfa = np.linalg.norm(v) if alfa > 0:

v = (1/alfa) * v

w = v.copy()

rhobar = alfa

phibar = beta

bnorm = beta

rnorm = beta

r1norm = rnorm

r2norm = rnorm # Reverse the order here from the original matlab code because

# there was an error on return when arnorm==0

arnorm = alfa * beta if arnorm == 0: print(msg[0]) return x, istop, itn, r1norm, r2norm, anorm, acond, arnorm, xnorm, var

head1 = ‘ Itn x[0] r1norm r2norm ‘

head2 = ‘ Compatible LS Norm A Cond A‘

if show: print(‘ ‘) print(head1, head2)

test1 = 1

test2 = alfa / beta

str1 = ‘%6g %12.5e‘ % (itn, x[0])

str2 = ‘ %10.3e %10.3e‘ % (r1norm, r2norm)

str3 = ‘ %8.1e %8.1e‘ % (test1, test2) print(str1, str2, str3) # Main iteration loop.

while itn < iter_lim:

itn = itn + 1 """

% Perform the next step of the bidiagonalization to obtain the

% next beta, u, alfa, v. These satisfy the relations

% beta*u = a*v - alfa*u,

% alfa*v = A‘*u - beta*v. """

u = A.matvec(v) - alfa * u

beta = np.linalg.norm(u) if beta > 0:

u = (1/beta) * u

anorm = sqrt(anorm**2 + alfa**2 + beta**2 + damp**2)

v = A.rmatvec(u) - beta * v

alfa = np.linalg.norm(v) if alfa > 0:

v = (1 / alfa) * v # Use a plane rotation to eliminate the damping parameter.

# This alters the diagonal (rhobar) of the lower-bidiagonal matrix.

rhobar1 = sqrt(rhobar**2 + damp**2)

cs1 = rhobar / rhobar1

sn1 = damp / rhobar1

psi = sn1 * phibar

phibar = cs1 * phibar # Use a plane rotation to eliminate the subdiagonal element (beta)

# of the lower-bidiagonal matrix, giving an upper-bidiagonal matrix.

cs, sn, rho = _sym_ortho(rhobar1, beta)

theta = sn * alfa

rhobar = -cs * alfa

phi = cs * phibar

phibar = sn * phibar

tau = sn * phi # Update x and w.

t1 = phi / rho

t2 = -theta / rho

dk = (1 / rho) * w

x = x + t1 * w

w = v + t2 * w

ddnorm = ddnorm + np.linalg.norm(dk)**2 if calc_var:

var = var + dk**2 # Use a plane rotation on the right to eliminate the

# super-diagonal element (theta) of the upper-bidiagonal matrix.

# Then use the result to estimate norm(x).

delta = sn2 * rho

gambar = -cs2 * rho

rhs = phi - delta * z

zbar = rhs / gambar

xnorm = sqrt(xxnorm + zbar**2)

gamma = sqrt(gambar**2 + theta**2)

cs2 = gambar / gamma

sn2 = theta / gamma

z = rhs / gamma

xxnorm = xxnorm + z**2 # Test for convergence.

# First, estimate the condition of the matrix Abar,

# and the norms of rbar and Abar‘rbar.

acond = anorm * sqrt(ddnorm)

res1 = phibar**2

res2 = res2 + psi**2

rnorm = sqrt(res1 + res2)

arnorm = alfa * abs(tau) # Distinguish between

# r1norm = ||b - Ax|| and

# r2norm = rnorm in current code

# = sqrt(r1norm^2 + damp^2*||x||^2).

# Estimate r1norm from

# r1norm = sqrt(r2norm^2 - damp^2*||x||^2).

# Although there is cancellation, it might be accurate enough.

r1sq = rnorm**2 - dampsq * xxnorm

r1norm = sqrt(abs(r1sq)) if r1sq < 0:

r1norm = -r1norm

r2norm = rnorm # Now use these norms to estimate certain other quantities,

# some of which will be small near a solution.

test1 = rnorm / bnorm

test2 = arnorm / (anorm * rnorm)

test3 = 1 / acond

t1 = test1 / (1 + anorm * xnorm / bnorm)

rtol = btol + atol * anorm * xnorm / bnorm # The following tests guard against extremely small values of

# atol, btol or ctol. (The user may have set any or all of

# the parameters atol, btol, conlim to 0.)

# The effect is equivalent to the normal tests using

# atol = eps, btol = eps, conlim = 1/eps.

if itn >= iter_lim:

istop = 7 if 1 + test3 <= 1:

istop = 6 if 1 + test2 <= 1:

istop = 5 if 1 + t1 <= 1:

istop = 4 # Allow for tolerances set by the user.

if test3 <= ctol:

istop = 3 if test2 <= atol:

istop = 2 if test1 <= rtol:

istop = 1 # See if it is time to print something.

prnt = False if n <= 40:

prnt = True if itn <= 10:

prnt = True if itn >= iter_lim-10:

prnt = True # if itn%10 == 0: prnt = True

if test3 <= 2*ctol:

prnt = True if test2 <= 10*atol:

prnt = True if test1 <= 10*rtol:

prnt = True if istop != 0:

prnt = True if prnt: if show:

str1 = ‘%6g %12.5e‘ % (itn, x[0])

str2 = ‘ %10.3e %10.3e‘ % (r1norm, r2norm)

str3 = ‘ %8.1e %8.1e‘ % (test1, test2)

str4 = ‘ %8.1e %8.1e‘ % (anorm, acond) print(str1, str2, str3, str4) if istop != 0: break

# End of iteration loop.

return x, istop, itn, r1norm, r2norm, anorm, acond, arnorm, xnorm, var

================================

校验假设:

虽然上面的实例算出了线性关系,但是我们怎么判断我们开始预设立得假设呢,就是我们是否要推翻假设,毕竟是假设,

假设未来一周我有一个亿,根据现实偏离太大,估计会推翻假设。

算了还是切入正题吧:

开始我假设了个模型:

![]()

我们需要校验这个假设,我们还要附加假定:

对于X的每一个固定值,所以的ε都相互独立,并且都服从均值为0,方程为σ方 的正态分布

![]()

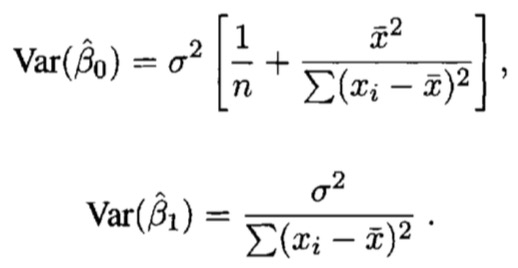

得到:

SSE为残差,n-2为自由度[自由度=观测个数-待估回归参数个数]

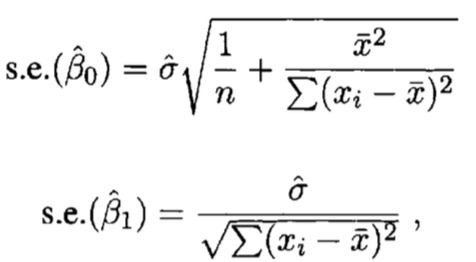

带入化简得倒,标准误差分别是:

![]() 的标准误差刻画了斜率的估计精度,标准误越小估计精度越高

的标准误差刻画了斜率的估计精度,标准误越小估计精度越高

本文出自 “similarface” 博客,请务必保留此出处http://similarface.blog.51cto.com/3567714/1860668

原文:http://similarface.blog.51cto.com/3567714/1860668